Year end resolution: Stop neglecting your cash flow

You know that you should be doing a cash flow spreadsheet. You keep hearing how important it is to your business, but for most small business owners, it’s just one more thing on a neverending to-do list.

I get that.

Who has time for projections when you’re trying to build the business, execute your marketing plan, manage your suppliers—and on and on. And when you finally make time for finances, your focus goes to catching up on outstanding bills, maybe organizing your receipts, and if you’re really lucky, reviewing your financials to date. Cash flow is neglected in favour of more pressing business matters.

But if you haven’t been paying attention to how money is flowing in and out of your business, you really need to start. Right now. It should be your #1 business resolution of the year.

Cash is the lifeblood of your business. Without it, your business doesn’t function. You can’t pay for your supplies, you can’t pay your employees, you can’t pay your rent. 30% of small businesses fail because of a lack of access to cash. And that’s a real bad time.

In contrast, when cash is flowing into your business, you’re able to pay for everything you need and then some. You can pay for upgrades to equipment, hire more staff to meet increased demand for your product or service, and you can invest in growing your business.

How cash flow affects your business

Being aware of your business’s cash flow is critical to knowing if you’ll be able to pay your bills when they fall due. You should regularly prepare three to six months of cash in and outflows so you’re able to get in front of any major purchases that need advance planning.

It’s also important to note HOW cash flows into your business. Is it solely from customers paying their bills? Do you draw on the banks through loans or overdrafts? Or sometimes do you need to borrow money from other sources to fund the day-to-day business needs?

For example, if you pay your employees and suppliers every two weeks, but invoice your customers on the last day of each month, do you know if you will have enough money in the bank to pay everyone by the end of the month? How dependant are you on your customers paying on time and immediately? What happens if someone is late with a payment?

If you aren’t sure of the answers to the above, then you definitely need to sit down and look at the state of cash in your business. The answer should be something along the lines of, “We borrow money from our line of credit or overdraft with the intention of following up on overdue payments”.

Learning how cash flows in and out of your business can keep your business from failing like those 30% of bankruptcies we mentioned earlier. So how do you do this?

Managing your cash flow

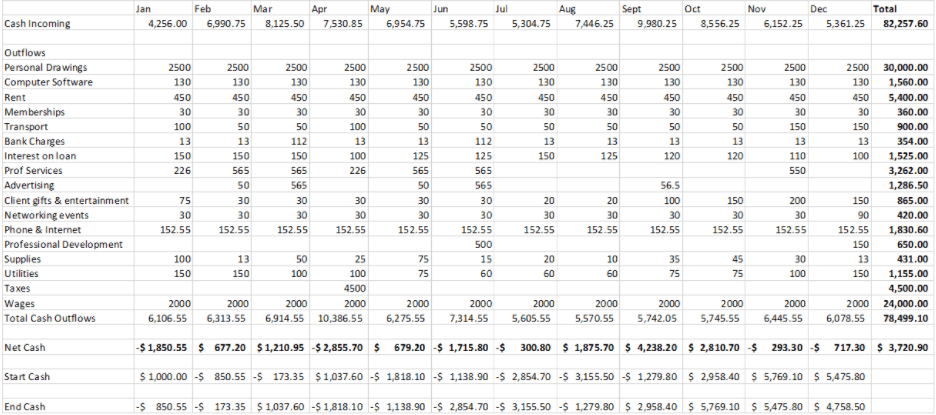

Preparing a cash flow statement isn’t as difficult as you might think. If you already use accounting software, you can run a report that shows your expenses in a particular month. If you don’t have accounting software, you can pull this data from your banking records in Excel. It’s a little more manual process, but you can prepare a spreadsheet in Excel or Google Sheets, like the one below.

Basically, you lump your spending into broad categories. Anything that isn’t strictly to do with business (i.e. your morning coffee, groceries, school or craft supplies for the kids, etc.) gets put into “personal drawings”, including any cash you withdraw from your business bank account to spend as you please.

I prepared this for a whole year, to give you an idea of the kinds of ups and downs your cash flow will go through. There are seasonal cash cycles to every business, and knowing what those look like will keep you from unwelcome surprises. You’ll notice there are some months when “end cash” is negative. That’s a big problem for your business, but knowing it’s coming means you can move things around, and change your payment options.

Maybe you can put that big expense on your credit card and pay it off a month later, or maybe you’ll set up a meeting with the bank to get access to a line of credit, overdraft or small business loan to cover the shortfall.

Really, once you know your numbers, anything is possible.

*While subscribed to Wave’s Pro Plan, get 2.9% + $0 (Visa, Mastercard, Discover) and 3.4% + $0 (Amex) per transaction for unlimited transactions during the offer period. After the offer ends: over 10 transactions per month at 2.9% + $0.60 (Visa, Mastercard, Discover) and 3.4% + $0.60 (Amex) per transaction. Discover processing is only available to US customers. See full terms and conditions.

See Terms of Service for more information.

The information and tips shared on this blog are meant to be used as learning and personal development tools as you launch, run and grow your business. While a good place to start, these articles should not take the place of personalized advice from professionals. As our lawyers would say: “All content on Wave’s blog is intended for informational purposes only. It should not be considered legal or financial advice.” Additionally, Wave is the legal copyright holder of all materials on the blog, and others cannot re-use or publish it without our written consent.